Post-Serta Uptier Evolution and When Holding Out Pays

Introduce Four Post-Serta Uptier Structures: Lessons from Mitel, Quest, Better Health, AMC, City Brewing, and Del Monte

On the last day of 2024, the U.S. Court of Appeals for the Fifth Circuit issued a landmark ruling that effectively shut down non-pro rata uptiers executed through the "open market purchase" exception. Prior to the decision, non-pro rata uptiers had arguably been the most popular form of liability management transaction. While the ruling clearly constrained how uptiers could be structured going forward, it didn't kill the strategy altogether.

In 2025, uptiers have remained common as restructuring bankers and lawyers adapted and found new ways to operate within the four corners of credit documents. According to CreditSights, in Q1 2025 alone, approximately 70.6% of liability management transactions (12 out of 17) that were launched or closed included some form of uptiering component.

After reviewing several recent restructuring cases that employed uptier structures, my takeaway is that every successful uptier needs to solve two core problems. First, the company must create a new super-priority, priming layer of debt. Second, it must ensure that this priming debt ends up in the hands of a selected group of lenders, rather than the entire syndicate.

In this article, I classify post-Serta uptiers into four main categories and walk through the contractual mechanics each relies on to accomplish these two objectives while minimizing litigation risk

Pre-emptive Amendments

Not all debt documents have very restrictive provisions. Through Q1 2025, roughly 44% leveraged loans still contained so-called "Serta loophole" language that allows the issuance of priming debt with only majority lender consent. In addition, many credit agreements historically did not treat pro-rata sharing as a sacred right.

A useful contrast here is the Mitel transaction, which was upheld on the same day the Fifth Circuit invalidated Serta. In Mitel, an ad hoc group of lenders approved amendments that facilitated the issuance of $156 million of new-money first-out debt. While the economic outcome resembled Serta, the legal footing was different. The Mitel credit agreement expressly permitted the borrower to "purchase loans by assignment", without imposing a pro-rata requirement on such purchases. As a result, the court found that the transaction complied with the contract as written.

For borrowers with similarly permissive documents, where amendments can be passed with majority consent and pro-rata sharing or subordination is not a sacred right, executing a non-pro rata uptier remains relatively straightforward. A majority lender group can first amend the credit agreement to authorize new super-priority debt, and then allocate that priming debt to participating lenders through an exchange or similar mechanism.

Yet it is also worth noting that, as non-pro rata uptiers have proliferated, many creditors have pushed to include so-called "Serta blockers" in credit agreements. These provisions typically take the form of requiring heightened—often unanimous—lender consent to permit subordination of existing debt. Despite this, uptier transactions remain prevalent even where such blockers are in place, largely because Serta blockers themselves have several structural weaknesses.

First, in many credit agreements, the Serta blocker is not itself treated as a sacred right. As a result, while the blocker purports to require universal consent to subordinate debt, the provision can sometimes be amended or removed with only majority lender consent. Second, many Serta blockers include carve-outs for DIP financing or other forms of rescue or emergency liquidity. This allows an ad hoc group to frame a transaction as a liquidity backstop rather than a hostile reprioritization, effectively squeezing through the exception. Third, some blockers focus narrowly on lien or payment subordination and fail to protect against structural subordination, leaving the door open for "drop-down and uptier" transactions (discussed further below).

Extend-and-Exchange

For particularly restrictive credit documents that eliminate the ability to execute an uptier through a straightforward amendment, restructuring professionals have developed more creative workarounds. One of the most notable post-Serta innovations is the extend-and-exchange structure designed to work even when pro rata sharing is treated as a sacred right.

In many credit agreements, the pro-rata sharing requirement applies only to loans within the same class. Extend-and-exchange exploits this feature through a two-step maneuver. First, the company offers a maturity extension to a subset of lenders. By consenting to the extension, these lenders move into a new tranche with a later maturity, effectively forming a separate class of debt. Second, the company exchanges the extended loans for newly issued super-priority debt, which primes the non-participating lenders. Because the super-priority debt is offered on a pro-rata basis to all lenders within the extended tranche, the transaction formally complies with the pro-rata sharing requirement.

A recent transaction that exemplifies this approach is Better Health. In January 2025, Better Health executed a liability management transaction in which a majority of its 2028 debtholders agreed to extend their maturities by one year, creating a new 2029 tranche not subject to the original pro-rata framework. The extended class then approved an exit consent that permitted the company to issue $113 million of new super-priority debt. A non-pro rata uptier was subsequently executed within the 2029 tranche, allowing the company to capture approximately $60 million of discount while improving liquidity.

Extend-and-exchange represents a novel response to the Serta decision, but it is not without limitations. Importantly, the structure still requires amendments to the credit agreement to authorize the issuance of priming debt, which may be impossible if the incurrence of super-priority debt is itself a sacred right. Additionally, because extend-and-exchange remains a relatively new technique, there is not yet a standardized "Better Health blocker." That said, lenders are likely to respond by pushing for protections such as: (i) making maturity extensions a sacred right—though this is difficult to negotiate given its impact on refinancing flexibility—and (ii) redefining pro-rata sharing to apply across all loans, rather than by class, or more clearly constraining what constitutes a separate "class" of debt.

Consensual Uptier

No matter how restrictive a credit document may be, an uptier can still be executed if creditors are broadly aligned and willing to participate in the transaction, receiving relatively balanced economics, and thereby effectively forgoing the option to litigate. These so-called "consensual uptiers" have become increasingly common over the past few years.

A full participation (or close-to-full) uptier typically occurs for several reasons. First, the SteerCo may prioritize making the transaction litigation-proof, particularly after recognizing how costly, uncertain, and time-consuming restructuring litigation can be. Second, creditors may share a common objective of supporting the company outside of chapter 11 as they have conviction in the business fundamental and believe they can get better recovery if the company sustains over the near-term headwinds.

However, full participation does not necessarily mean pro-rata treatment. In most cases, a consensual uptier still differentiates between the ad hoc group and non–ad hoc lenders in order to reward the former for providing new money and anchoring the transaction. The key distinction is that, unlike more aggressive uptiers such as Serta or Incora, the economic gap between in-group and out-group lenders is typically much narrower.

The enhanced economics for the ad hoc group usually take the form of higher exchange rates, higher interest coupons, and/or the opportunity to provide new-money super-priority financing. Non–ad hoc lenders, while treated less favorably, often conclude that the downside of participating is preferable to the alternative. Given how costly, uncertain, and time-consuming restructuring litigation can be, the expected cost of litigation frequently exceeds the economic concession required to participate in the transaction.

A good example of a consensual uptier is Quest Technology. In May 2025, the Clearlake-backed technology company faced a liquidity crunch and executed an uptier transaction with full lender participation. An ad hoc group provided new money and exchanged its claims at 92 cents on the dollar into super-priority second-out debt. Non–ad hoc lenders, meanwhile, were permitted to exchange 70% of their claims into the same super-priority tranches, albeit at a 23% haircut. While this resulted in roughly a 15-cent differential in recovery between the two groups, the disparity was far less punitive than in earlier, heavily litigated uptiers where only a narrow subset of lenders participated and captured the entirety of the upsides.

Drop-down and Uptier

As discussed earlier, extend-and-exchange structures may not be practical when subordination is treated as a sacred right, effectively blocking the issuance of priming debt through amendments. In those cases, restructuring professionals have turned to an alternative: the "drop-down and uptier".

In a drop-down transaction, the company exploits available investment capacity to move valuable assets out of the existing lenders' collateral pool and into an unrestricted subsidiary or a non-guarantor restricted subsidiary. Using this newly isolated collateral, the company can then raise new money that is structurally senior to the existing debt. Because the priming debt is issued at a different entity, rather than at the original borrower, the company often does not need to amend the existing credit agreement. As a result, the structure can bypass even the most restrictive uptier blockers, including those that treat subordination as a sacred right.

Drop-down and uptier transactions have become increasingly common in recent years. In August 2024, canned food producer Del Monte executed a high-profile liability management transaction in which it transferred most of its operating assets to an unrestricted subsidiary, enabling the company to raise $269 million of new-money super-priority first-out debt. An ad hoc group holding approximately 57% of the existing term loan then exchanged its claims into super-priority second-out debt at par, while non–ad hoc lenders were offered the opportunity to exchange into second-out and third-out tranches, also at par.

Similarly, in April 2024, beverage manufacturer City Brewing completed a drop-down transaction by transferring its brewing facilities into a non-guarantor restricted subsidiary. Notably, the structure also included a double-dip feature for its $122 million new-money facility, providing participating lenders with multiple claims against the capital structure.

A drop-down and uptier promises some unique benefits compared to other uptiers: 1) as long as there is ample investment capacity, the company can effectuate the transaction without locking in supermajority lender support, and 2) the participation incentive may be even stronger than in traditional uptiers. Rather than simply being pushed down the payment waterfall by new priming debt, non-participating lenders are effectively stripped of collateral altogether as assets are transferred out of the existing lien package.

That said, drop-down and uptier transactions also come with meaningful drawbacks. They are significantly more complex than a vanilla amendment or exchange, which increases execution risk and makes the process more time-consuming. More importantly, the added structural complexity often invites litigation across multiple dimensions of the transaction. In the Del Monte case, for example, holdout lenders did not challenge the transaction on non-pro-rata grounds, but instead litigated the transfer of assets into an unrestricted subsidiary. Ultimately, the company backed down and was forced to pay the dissenting lenders out at par.

The New Economics of Holding Out

The Serta decision only closed one loophole but it did not eliminate uptiers as a restructuring tool. While the mechanics differ across all post-Serta transactions, the objective is the same: create the priming loan and allocate them selectively. While pre-emptive amendment exploits the contractual weakness to accomplish that, consensual uptier incentivizes non-ad hoc group participation by offering better economics; extend-and-exchange structures work around pro-rata sharing through class formation, and drop-down uptiers bypass priority restrictions by shifting assets and creating structural seniority.

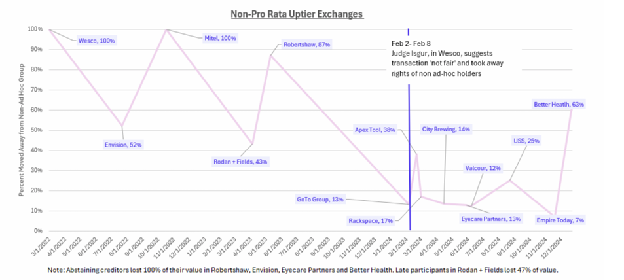

Together, these approaches point to a broader shift in liability management transactions toward structures that are more inclusive and less overtly aggressive. While economic differences between ad hoc and non–ad hoc lenders still exist, they are far less pronounced than in earlier transactions such as Serta or Incora, where the outcome was effectively winner-takes-all, because of the fear of litigation and the need to lock in mass participation for amendment. This evolution leads to a counterintuitive but important observation I want to discuss in this article that in certain LMEs, holdout lenders may end up achieving the strongest recoveries.

As the graph shows, as uptier evolves, the value extracted from non-ad hoc groups has progressively declined. In Serta/Incora, the ad hoc group emerged at the very top of the capital structure and was fully protected by collateral following the reprioritization of claims. As a result, those lenders were largely indifferent to a near-term Chapter 11 filing, since they would expect to recover at or near par regardless.

By contrast, in more recent uptiers, the incremental recovery uplift for the ad hoc group is meaningfully smaller. Short of full recovery, participating lenders are effectively forced to form a closer partnership with the company and ties their outcomes to the success of an out-of-court solution and a potential operational turnaround (which is very rare in reality). In this setting, holdout lenders typically sit in the earliest-maturing tranche of the capital structure. Because participating lenders have little incentive to trigger a bankruptcy over a relatively small holdout position, they are often willing to contribute additional capital to facilitate a payoff of the holdouts. As a result, holdout lenders can sometimes extract better recoveries than might otherwise be expected.

A clean real-world example of this dynamic is AMC's 2024 LME. The drop-down and uptier transaction was intentionally broad and relatively inclusive, with limited value transfer to the ad hoc group, meaning participating lenders did not emerge fully protected and instead tied their outcomes to AMC staying out of court. In that setting, the small group of left-behind second-lien notes due in 2026 became the inside maturity and a practical roadblock. Because neither the company nor participating lenders had an incentive to trigger a Chapter 11 over a modest holdout position after pushing most maturities to 2029, the market began to price in an eventual payoff. As a result, those left-behind 2Ls rallied sharply and traded toward par.