The Bubble That Doesn't Pop - Until It Does

Private Credit emerged in the wake of the 2008 Global Financial Crisis as banks retrenched from lending, and the asset class really boomed during the COVID-19 era of ultra-low interest rates, when defaults were scarce. Yet, this nearly $2 trillion asset class has still not been tested by a full credit cycle. With a rising tide of defaults and workouts, however, it’s likely that private credit will be taking its first big test in the next three to five years.

Warm Winds in Credit, With a Breeze of Caution

Credit investors, both in the public and private spaces, have been pretty optimistic.

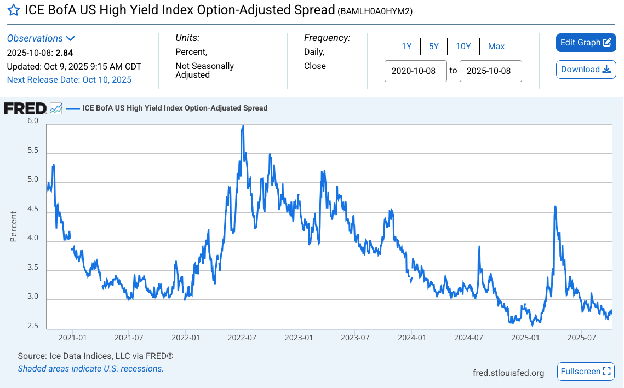

The High Yield Index Option-Adjusted Spread was 284 basis points on October 8, 2025. The spread measures the difference in yield between high yield corporate bonds and the risk-free government bonds. To contextualize this, spreads below 300 bps are narrower than normal ranges; historically, high yield spreads have averaged between 350 - 600 bps. The current levels are near multi-decade lows. The last time we saw ~300 bps was in mid-2021 when the global economy and corporate earnings were recovering strongly from the COVID-19 shock, leading to robust fundamentals and expectations of low default rates. The low spread generally indicates that investors are taking a risk-on mode: they see limited risk in their investment and, correspondingly, demand lower returns.

Similar sentiment was shared by private credit investors. Private credit has exploded into a $1+ trillion asset class following the retrenchment of banks in providing loans after the 2008 financial crisis. Private credit spreads have also tightened in 2025, especially in the US direct lending market. Best-in-class unitranche transactions are now pricing at around 475 bps, and the spread premium between mid-market and upper middle market deals narrows from 200bps in 2024 to just 100bps in 2025. In September 2025, a consortium consisting of Blackstone, Blue Owl, and Ares repcied $2.65 billion in private credit for Permira-owned website builder Squarespace at a 375 bps premium, the lowest spread ever for a PE-backed private credit deal.

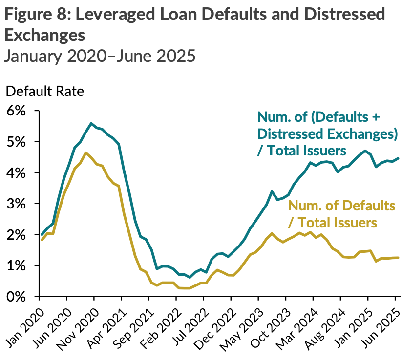

But if we step back for a second, are we really living in the best time ever? maybe it does not seem that way - maybe. Interest rate remains high despite a recent cut. The supply chain is not stabilized. Many companies face pressure from rising prices of raw materials. More companies are filing for bankruptcy despite the rising popularity of out-of-court restructuring. According to Cornerstone Research, a total of 117 large companies filed for bankruptcy in the last 12 months (2H 2024 - 1H 2025), an increase of 4% from 113 in the prior 12 months, which is 44% above the 2005 - 2024 annual average of 81 bankruptcies. Leveraged loan default rate is trending upward, displaying quite the opposite movement to the high yield bond spread.

Some industry reports point out that as investor demand surged and deal volume remained limited, private credit funds have been under pressure to deploy capital, leading to compression in spreads. The recent First Brands drama further produced some cautionary signals to private credit investors.The company leaned on off-balance-sheet financing by collateralizing working-capital assets like receivables, and investors underestimated the risk amid accounting sleights. Millennium, notably, took about a $100 million hit on short-term loans to First Brand. The drama sent a cautionary signal that over-engineering leverage on non-durable assets could mask fragility rather than reduce it.

Is LME Frontier Moving to Private Credit

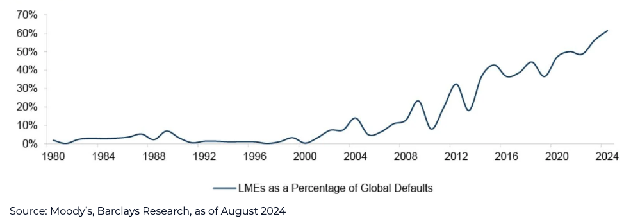

With that backdrop and the rise of (sometimes aggressive) Liability Management Exchanges over the past decade, the natural question is whether we will see more LMEs targeting companies financed by private credit.

LMEs represent over half of all defaults

We’ve already seen two examples of this dynamic: Alacrity and Pluralsight. Pluralsight is a technology company that provides technology training solutions for businesses, specifically in the IT sector. The company was taken private by Vista Equity Partners in early 2021 at a valuation of $3.5 billion. Vista Equity Partners was very ambitious when underwriting the deal, but the later topline growth and EBITDA expansion were lower than expected. Meanwhile, the sharp rise in rates since 2021 pushed up interest costs on its floating-rate debt (roughly SOFR + 800 bps). Finally, in 2024, it seemed that an LME was inevitable if Pluralsight wanted to avoid filing for bankruptcy

The Pluralsight LME was very interesting: Pluralsight engaged in a drop-down transaction which was pioneered by J. Crew in 2017. A drop-down is basically the company exploiting the investment baskets to transfer valuable assets to an unrestricted subsidiary. The company then uses these unencumbered assets to attract fresh capital which primes the legacy secured debt. What’s revolutionary in Pluralsight’s case was that instead of moving its valuable IP to an unrestricted subsidiary, Pluralsight used a non-guarantor restricted subsidiary. It did so because the credit document had a J. Crew blocker, so the non-guarantor restricted sub was the available alternative, even though the non-guarantor restricted sub still sit within the credit box so the amount of new capital raised was limited by the lien capacity outlined in the existing credit doc. Nevertheless, Pluralsight was still able to raise $170 million of new debt, $50 of which came from Vista Equity Partners. The private credit lenders (consisting of Blue Owl and Ares), were left with effectively no collateral.

Covenant Dilution and Bespoke Loopholes

Some people believe that Pluralsight sets the stage for future aggressive LMEs to companies financed with private credit. One of their arguments centers around covenant erosion - the steady weakening of lender protections in loan agreements.

Until about five years ago, a major distinction between syndicated loans and private credit loans was that syndicated loans were generally cov-light, meaning they did not have maintenance covenants that periodically tested the financial health. Private credit loans, on the other hand, tended to have multiple financial covenants in lender-friendly loan agreements, giving creditors early signs when borrowers’ performance deteriorated. Covenants are also important in the sense that they could pre-empt potential aggressive LME from being done against them. For example, after Serta’s non-pro rata uptier transaction, some credit documents included a Serta blocker that prevented priming of new money that leapfrogs existing lenders by giving a clearer definition of “Open Market Purchase” or treating priming liens as a sacred right. Following Pluralsight’s dropdown, likewise, some private credit demanded a block that prevents a company from transferring assets to a non-guarantor restricted sub.

But over time, as more private credit investors entered the market and pressure to deploy capital increased, the competitive pressure made some lenders increasingly willing to waive covenant protection. As the chart shows, most senior loans now lack meaningful covenants. As the default cycle unfolds, this covenant erosion will be tested. Maybe covenant-lite loans will delay defaults and give companies time to recover, or maybe they will open the door to tougher LMEs on creditors.

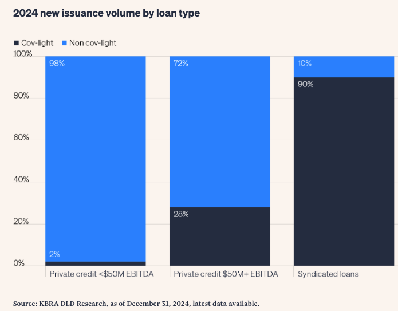

People who are optimistic about private credit will argue that, despite a gradual weakening of covenant protection, private credit loans are still much lender-friendly than broadly syndicated loans, especially in the middle market with loan values lower than $500 million, as the graph shows. Therefore, it was much more difficult to do aggressive LMEs against private credit.

Proliferation of Club Private Credit Deals

Another trend that may support the viewpoint that LMEs will hit the private credit market is the proliferation of larger syndicate groups within private credit deals. The percentage of issued private credit deals with five or more lenders grew from 0.5% in 2014 to 7.5% in 2024. As syndicate size increases, the lender group becomes more fragmented and less cohesive. With fewer lenders, negotiations are direct and relationships tend to be collaborative; with more lenders, coordination becomes challenging, which can invite divisive actions such as LMEs or lender-on-lender violence.

Moreover, many credit agreements allow significant amendments or up-tier transactions with the consent of a simple majority (often 51%). In larger syndicates, a majority can be formed more easily, potentially at the expense of minority lenders, enabling LMEs that favor certain groups and subordinate non-participating lenders.

Innovation and Resilience of Private Credit

Despite structural risks and gradual saturation of the market, the private credit market still offers numerous opportunities, but the ability to capitalize on them through sound structuring and effective risk minimization is the key differentiator between a good and a mediocre investor. For example, one high-conviction pocket in private credit is asset-based lending. Blackstone’s $7.5 billion debt financing to CoreWeave in 2024 is a good example of how disciplined structuring can earn attractive returns. CoreWeave is a fast-growing AI infrastructure provider that spends huge sums upfront on NVIDIA GPUs and data centers before collecting payments from clients. So the company, in a traditional sense, is not a good target for private credit investors who are more comfortable with lending money to companies that are established and have stable cash flow. Blackstone, however, came up with an innovative financing structure. CoreWeave created a special purpose vehicle (SPV), CoreWeave Compute Acquisition Co. IV, LLC, as borrower. Blackstone structured the debt such that the SPV pledged the GPUs plus service contracts with large and credit-worthy customers like Microsoft as collateral. Because the SPV is a dedicated borrower with that collateral, Blackstone enjoys first priority claims on the pledged assets, notwithstanding that it was only in the mezzanine position in CoreWeave's consolidated capital structure.

The structural advantage of private credit is the broad mandate. Unlike private equity, whose leveraged buyout model struggles with high interest rates and poor exit conditions, private credit has the flexibility to generate strong opportunities across different market cycles. For example, during 2021 and 2022, when the pandemic hit the economy hard, distressed funds generated a net IRR of over 40%. 2023 onward as the economy gradually stabilized, distressed funds have struggled while direct lending delivered solid returns of mid-teens. Given today’s uncertainty, this adaptability underscores the importance for multi-strategy investors to adjust their focus within the asset class.

Ultimately, the coming cycle of increasing economic uncertainty and corporate default risk will not decide whether private credit survives, but what form it will take. This is consistent with BlackRock’s 2025 private-market outlook, which observes wide performance dispersion in private debt. The asset class is entering its first genuine test of discipline, where credit outcomes will depend less on liquidity and more on structure, governance, and underwriting. If disciplined lenders emerge stronger while yield-chasers falter, private credit will exit this stress not as a burst bubble, but as a durably institutionalized pillar of modern finance.