Fiber Dreams, Debt Nightmares: Out-of-court Restructuring of CommScope and Lumen Technologies

Think of the telecommunication network like a huge system of highways. Now picture traffic jams and aging bridges while engineers work on upgrades in real time. That’s what is happening in telecommunication industry today: vast networks demanding upgrade, massive debt loads, and new ownership signs going up by the week. The telecommunication industry has entered a stressful transition period marked by distressed M&A and high-stakes restructuring, and their growing pains are influencing everything from the price we pay to the speed we stream.

This piece is my attempt to understand the wave of restructuring in today’s telecom world. I’ll start with a brief overview of how the industry is set up, then look at why so many telecom companies are under pressure from heavy debt and rising costs. Finally, I’ll look at how specific firms are responding, highlighting two recent restructurings and distressed deals that are quietly reshaping the industry.

The Telecom Squeeze

When I open TikTok and blaze through ten videos in just five seconds, there is a long value chain at play behind the scenes. It can be simplified into 3 layers:

- Network infrastructure owners

They build and maintain physical networks: copper cables, fiber optics lines, and cell towers that carry voice, data, and video. They make money through wholesale leasing of network capacity to retail service providers. Hence, their business models typically feature large, upfront capital expenditure followed by predictable maintenance costs and long-term contractual revenue streams.

- Network equipment vendors

They design and manufacture the essential hardware and software engines that allow telco networks to run: routers, antennas, fiber-optic transmission gear, and the digital control platforms that direct all data traffic. Their business models rely on waves of technology upgrades, like the shift to 5G and cloud-based networking which create demand for new products, large initial sales, and recurring service contracts. Hence, network equipment vendors usually experience revenue spikes in upgrade cycles but the competition is fierce.

- Retail Telcos & service providers

Think of this sector as the big names we all know, AT&T, Verizon, and others, which sell phone plans that bundle network access with digital services for a monthly fee. But it’s not just about consumers. Plenty of companies here focus on businesses too, offering things like cloud hosting, video, and smart services. An interesting restructuring example in this vertical is Mitel. The problem for retail telcos is that growth has stalled: subscriber revenue stays flat while costs keep climbing as companies increasingly bundle streaming, cloud storage, and value-added services to attract/retain customers. Hence, A major value creation method in this mature market we see recently is consolidation with the intent to extract cost synergies.

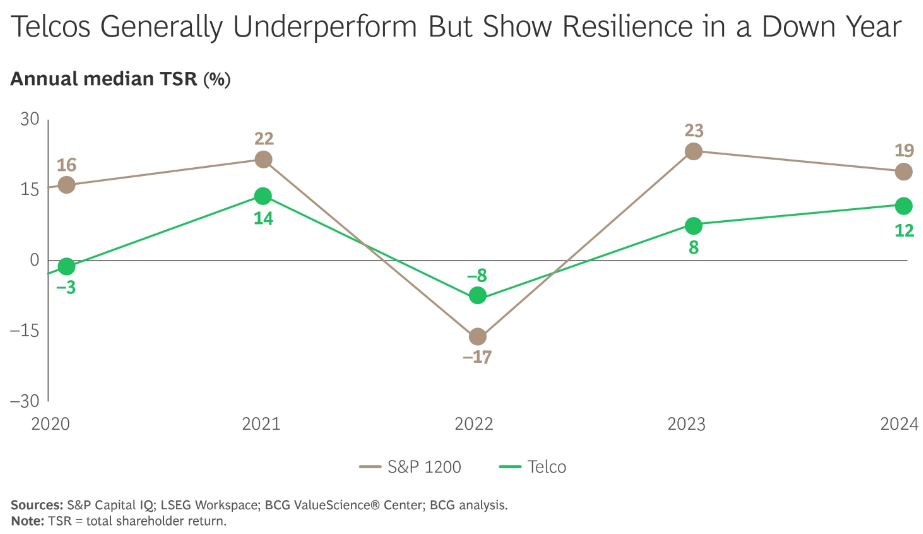

The space of telecommunication is traditionally dominated by hyperscalers that are vertically integrated throughout the value chain. For decades, industry wisdom suggested that only outsized telcos could generate outsized returns. But lately, that playbook hasn’t aged well. According to BCG, in the five years from 2020 to 2024, the telcos delivered a disappointing annualized total shareholder return of about 4%. That’s far below the 12% five-year annualized return of the S&P 1200 index of global stocks, leaving telecommunication 31st out of 33 industries BCG tracks.

It may not sound like the most exciting industry at first glance, but it’s often where some of the most interesting restructuring stories happen.

It may not sound like the most exciting industry at first glance, but it’s often where some of the most interesting restructuring stories happen.

It’s worth noting some key trends that make it so difficult to run telcos.

Increasing Capex requirement and capital intensity. Telcos, especially network infrastructure owners, are not unfamiliar with high fixed costs. But in the past five years, the ground has shifted with the transition from copper to fiber-optic lines, which deliver far greater bandwidth and longer transmission distances. AT&T announced that it will phase out copper-based network services across most of its territory by 2029, saving $6 billion annually. However, those savings come only after a massive upfront bill. Laying just one mile of fiber in the U.S. costs between $40,000 and $80,000, and there are still 30 to 50 million copper landline connections left. That’s a hundred-billion-dollar project, and telcos are loading themselves with debt well before seeing the payback.

Rising rates have only made the debt burden heavier. Many telcos loaded up on borrowing five years ago to finance fiber rollouts, only to watch the Fed hike rates from near 0% to over 5% by 2024. The result: interest costs spiked, covenants strained, and all this came on top of slowing sales, tougher competition, and a saturated market. In 2024, telcos posted a median ROIC of just 6.7%, falling short of their 7.1% WACC, meaning capital invested is now destroying, not creating, value.

To survive and adapt, telcos are being forced into bold changes. The once all-in-one giants now see the need to slim down their balance sheets and concentrate on the downstream segment with higher margins and lighter capital demands. That’s why we’ve seen a wave of high-profile asset sales and spin-offs where vertically integrated telcos offload massive network assets to infrastructure investors in exchange for capital and debt relief. An example is Telecom Italia’s 2024 sale of its legacy fixed-line network to a KKR-led consortium for $20 billion. Moves like these often blur into distressed M&A, which we’ll get into later.

To illustrate how telcos struggle and respond to the trends, this article looks at two cases: CommScope, a hyperscaler that shed $10 billion worth of cable assets to repair its overleveraged balance sheet; and Lumen Technologies, a network operator that had to undergo massive out-of-court restructuring to right-size its debt the hard way.

CommScope’s $10 Billion Do-Over

CommScope Holding Company, Inc. is a global provider of telecommunication infrastructure solutions. It has three major business lines:

- Connectivity and Cable Solutions (CCS) produces the physical cables and connectivity hardware, including fiber-optic and copper cables, connectors, and related infrastructure used in data centers, residential broadband, and video distribution networks. In FY 2024, CCS achieved $2.8 billion of sales, representing 67.1% of aggregate income.

- Networking, Intelligent Cellular & Security Solutions (NICS) provides wireless networking equipment for enterprises and service providers. Its portfolio includes Wi-Fi access points, LTE/5G cellular equipment, network switches, and related security and analytics software. In FY 2024, NICS generated $550 million of sales, representing 13.1% of total revenue.

- Access Network Solutions (ANS) supplies broadband distribution and transmission systems used by cable and telecom providers. Products include cable modem termination systems (CMTS), video infrastructure, and cloud-enabled platforms that allow service providers to deliver high-speed internet and video across residential and metro networks. In FY 2024, ANS recorded $820 million of sales, accounting for 19.7% of total revenue.

If you recall the telecommunication industry value chain just mentioned, CommScope is a perfect example of a vertically integrated giant: CCS delivers the core network infrastructure, while NICS and ANS operate further downstream, offering network equipment and enterprise-focused software and services.

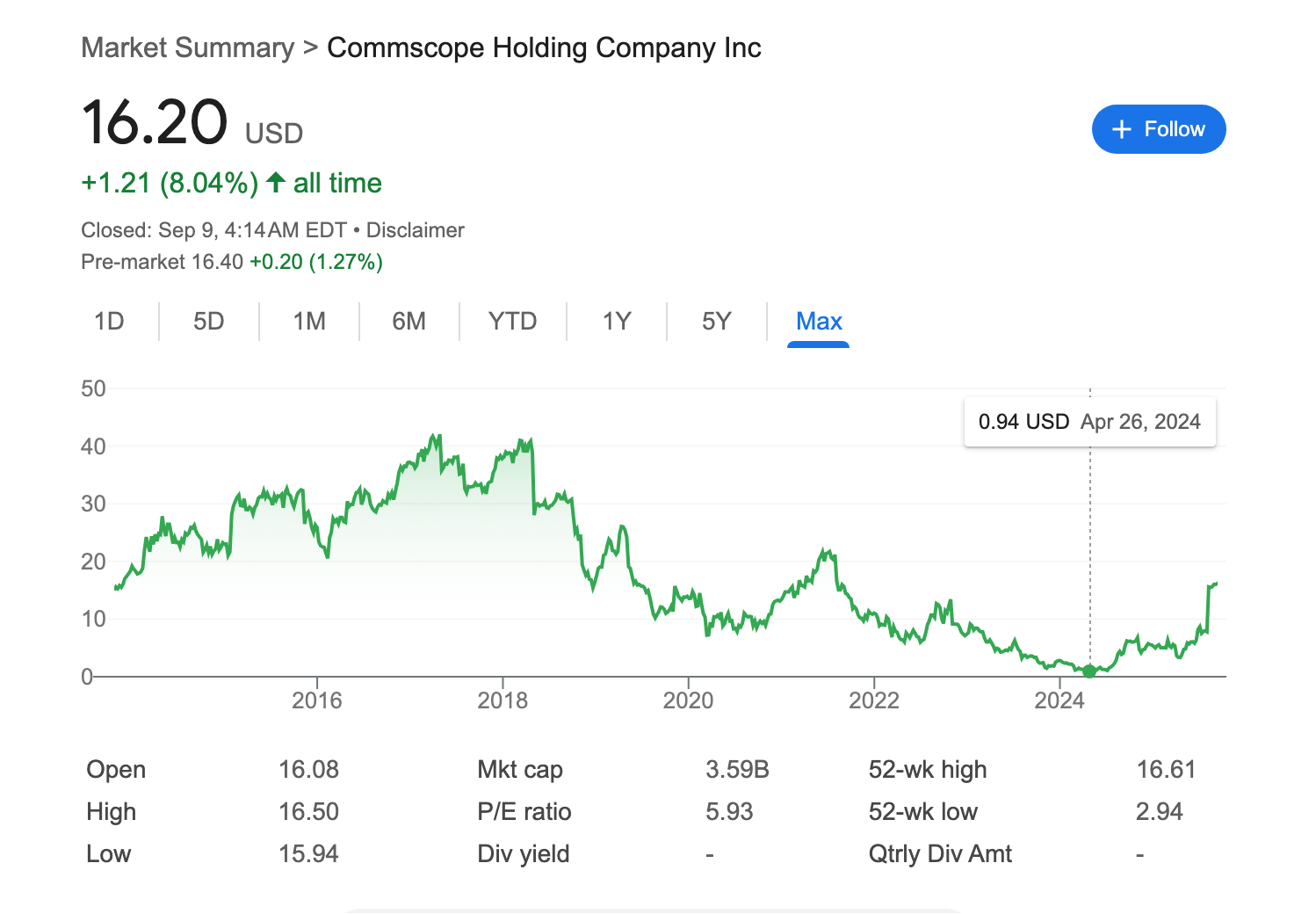

Yet CommScope’s strong revenue base, global scale, and vertically integrated model could not shield it from mounting financial pressures. Since 2019, CommScope has begun showing early signs of financial strain, marked by credit downgrade, stock trading down, and goodwill impairment. Those strains culminated in August 2025, when the company took its most dramatic step: selling its largest and legacy division, CCS, to Amphenol for $10.5 billion. Once the backbone of the business, CCS was divested to cut debt and salvage a stock that had plunged to $0.94 in mid-2024, levels that signaled investors were already bracing for bankruptcy. Behind that dramatic divestiture lies a longer story of mounting industry pressure and strategic miscalculations of its own making.

ARRIS Acquisition

CommScope began in 1976 when Frank Drendel and Jearld Leonhardt bought the “Comm/Scope” cable product line out of Superior Continental Cable and spun it into a standalone company in North Carolina. Over the 2000s–2010s, CommScope deepened its role as a maker of fiber and copper cables, connectors, and racks. The company IPOed on NASDAQ in October 2013.

A pivotal moment in CommScope’s trajectory came with the acquisition of ARRIS in April 2019. Until then, CommScope had been primarily a hardware provider of cable and fiber-optic lines. ARRIS brought a full suite of broadband and video equipment used by cable and telecom operators, along with networking management solutions for businesses, schools, and large venues. Management expected the deal to double CommScope’s addressable market to more than $60 billion, expand into higher-growth service-provider and enterprise markets, deliver over 30% accretion to adjusted EPS in year one, and generate more than $150 million in annual cost synergies within three years. CommScope paid $31.75 per share in cash, a 27% premium, which valued ARRIS at $7.4 billion.

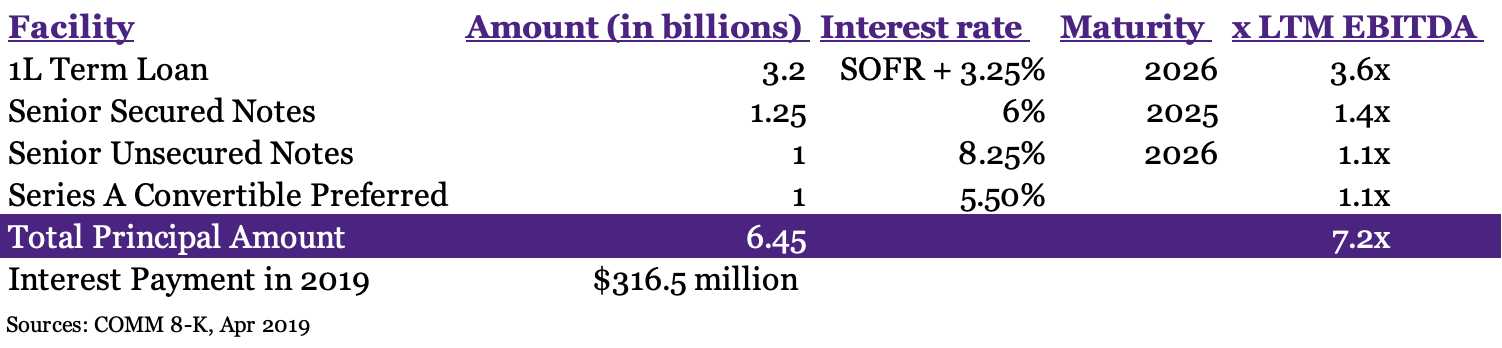

Looking back, was it a good acquisition? Strategically, yes, to some extent. The deal gave CommScope the foundation for its NICS and ANS segments, which became the company’s major focus today after shedding CCS. Was the acquisition financially sound? I do not think so. To finance the acquisition, CommScope took on $6.45 billion of new debt. The financing package is detailed below. Spoiler alert: Some of these facilities would go on to give CommScope’s management serious headaches in the years ahead.

The ARRIS acquisition more than doubled CommScope’s debt, pushing leverage from under 5× in 2018 to over 11× in 2019. S&P downgraded CommScope’s rating to B+ upon closing the transaction. While sales doubled after the acquisition, profitability did not follow suit. Adjusted operating margin collapsed from 16% to just 2%, underscoring the challenges of integrating ARRIS efficiently and realizing the cost synergies management had projected.

The ARRIS acquisition more than doubled CommScope’s debt, pushing leverage from under 5× in 2018 to over 11× in 2019. S&P downgraded CommScope’s rating to B+ upon closing the transaction. While sales doubled after the acquisition, profitability did not follow suit. Adjusted operating margin collapsed from 16% to just 2%, underscoring the challenges of integrating ARRIS efficiently and realizing the cost synergies management had projected.

Closer scrutiny reveals the economic strain of the ARRIS deal. In 2019, CommScope reported five business segments, three of which stemmed from ARRIS and together generated $4.8 billion of revenue. With ARRIS historically operating at a 6% margin, these assets would have produced roughly $290 million in operating profit. This was not even sufficient to cover the $316 million of additional interest expense incurred to finance the acquisition, let alone other costs related to the acquisition like the integration cost.

Closer scrutiny reveals the economic strain of the ARRIS deal. In 2019, CommScope reported five business segments, three of which stemmed from ARRIS and together generated $4.8 billion of revenue. With ARRIS historically operating at a 6% margin, these assets would have produced roughly $290 million in operating profit. This was not even sufficient to cover the $316 million of additional interest expense incurred to finance the acquisition, let alone other costs related to the acquisition like the integration cost.

More importantly, the heavy balance sheet left behind by the ARRIS acquisition reduced CommScope’s financial and operational flexibility, leaving it especially vulnerable when industry-wide headwinds struck in the years that followed.

Macro Headwinds

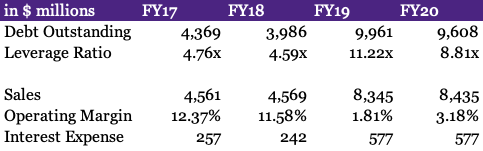

CommScope’s struggles cannot be understood without looking at the broader backdrop of the telecommunications sector. After a period of post-COVID build-outs, telecom operators began to cut back on spending in 2023 and 2024, slowing both 5G deployments and fiber optics cable rollouts. Customers had also over-ordered equipment during the pandemic and spent much of 2023 digesting inventory, which sharply reduced demand for CommScope. One reason behind the trend was that telcos took on massive debt to finance their capex when the rate was zero, and they soon found themselves financially strained as the Fed aggressively raised the interest rate since 2022.

The financial impact was stark. Revenue dropped 23% in 2023 to $5.8 billion, followed by another 8% decline in 2024 to $4.2 billion. The downturn affected all of CommScope’s business lines: NICS and ANS, both inherited from ARRIS, suffered the sharpest declines as operators delayed broadband and Wi-Fi investments, while CCS held up better thanks to demand from data centers. Adjusted EBITDA fell from $821 million in 2022 to $664 million in 2023 before stabilizing at $700 million in 2024 which was still far below pre-COVID levels. To reflect the lower-than-expected profit-generating ability of its assets, CommScope recognized a $571 million goodwill impairment across its ANS and CCS segments, and another $1.12 billion impairment of the ANS segment.

Restructuring Efforts

From 2019 to 2024, CommScope consistently recognized negative net income while its interest expense ran at roughly twice its operating income. The free cash flow remained barely positive, but it was negligible relative to the company’s debt burden. For management and creditors, the message was clear: leverage was unsustainable, and refinancing risk loomed large. It looked increasingly likely that the company would have to file for bankruptcy, as reflected by its share performance, which started trading downward when the ARRIS acquisition was announced.

The major issue concerning the management was that CommScope faced huge near-term maturity walls: $1.25 billion of senior secured notes due 2025 and $2.7 billion 1L term loan due 2026 - all borrowed in 2019 to finance the ARRIS acquisition.

Refinancing these facilities was not easy, given their size and CommScope’s deteriorating credit profile. Ultimately, CommScope struck a deal with existing first-lien lenders, Apollo and Monarch Alternative Capital. The package included two facilities:

$3.15 billion 1L term loan matures Dec 2029: SOFR + 4.5% - 5.5% (grid pricing based on 1L net leverage); 50% excess-cash-flow sweep, and required prepayment from certain asset sales and specified refinancing debt

$1 billion 1L senior secured notes mature Dec 2031: fixed 9.5% coupon; Asset-sale offer to repurchase at 100%

From the lenders’ perspective, forcing a default offered limited upside. As first-lien creditors with collateral over most of CommScope’s fixed assets, they were already well covered and likely to be repaid close to par in bankruptcy. Instead, backing an amend-and-extend allowed them to safeguard their existing exposure while locking in richer economics, as the new loan came with rich pricing and stronger protections.

In parallel with its refinancing, CommScope began shedding parts of the business. In July 2024, it struck a deal to sell its Outdoor Wireless Networks (OWN) segment and Distributed Antenna Systems (DAS) business to Amphenol for $2.1 billion in cash. The deal closed in February 2025, and the proceeds were used to fully pay off its revolving credit facility, retire its 6.00% Senior Secured Notes due 2026, and partially retire its 4.75% Notes due 2029

Yet, despite these efforts, CommScope’s restructuring was far from complete. Its capital structure at the end of FY 2024 suggested that CommScope still exhibited characteristics of a distressed company. The leverage ratio remained high, and the company faced daunting maturity walls in 2027 and 2028, when $1.6 billion and $641 million of debt would come due. The company did not have enough liquidity to pay down those obligations, and it was difficult to refinance because nearly all its assets were encumbered, and no lender was willing to extend unsecured credit to the company, given its deteriorating credit profile. Even a debt-for-equity swap was unrealistic, as the company’s equity value stood at only a fraction of the outstanding principal. Against this backdrop, another major asset sale appeared to be the only viable path forward.

CCS ultimately emerged as the asset best positioned to unlock value: it was attractive to buyers, enjoyed a strong valuation multiple, and could generate enough proceeds to address CommScope’s debt burden. As the company’s largest division, CCS generated $2.8 billion of sales in 2024. The division sat directly in the growth areas investors were most eager to buy into, namely fiber and connectivity for data centers, IT datacom, broadband, and building infrastructure. Amphenol, the eventual buyer, was actively scaling into the AI-driven data-center build-out and pursuing consolidation in the interconnect space, and CCS was a perfect fit. Amphenol underscored this value by projecting that CCS would deliver $3.6 billion of revenue and 26% EBITDA margins in 2025 under its ownership, which justified the $10.5 billion all-cash price.

Advised by Evercore, CommScope is expected to close the CCS sale in the first half of 2026. The company has announced plans to use the $10 billion of proceeds to repay all outstanding debt and redeem the Carlyle preferred equity, effectively transforming a stressed balance sheet into a clean one. The announcement lifted its share price back to around $16, implying a P/E ratio of 6. Still, I do not believe the stock will ever regain its 2019 valuation of 10× P/E, given the divestiture of its most profitable business. This contrast underscores how the 2019 ARRIS acquisition made little financial sense as CommScope paid roughly 12× earnings. Therefore, CommScope’s downfall is a good example of how an ill-timed, ill-informed acquisition in a difficult market can destroy even an industry giant.

Lumen’s Long Road to Deleveraging

CommScope’s story is dramatic, but it isn’t unique. Another telecommunication giant that experienced similar industry-wide pressures and operational setbacks - though with a different path to survival - is Lumen Technologies. Pari Passu newsletter has an excellent deep-dive on Lumen’s liability-management transactions. My goal here is simply to build on that work with a few details I found interesting and to share some of my own observations about Lumen’s restructuring.

In brief, the story of Lumen traces back to its earlier identity as CenturyLink, a name it carried until its rebrand in 2020. Founded in the 1930s, CenturyLink evolved into a major player in U.S. telecommunications infrastructure, offering primarily copper-based broadband connections that served both residential and business customers.

By the mid-2010s, fiber optics had emerged as the superior infrastructure poised to replace legacy copper networks. Rather than build its own fiber technology, CenturyLink chose to buy scale, completing its acquisition of Level 3 in 2017. Level 3 was a global, fiber-rich provider focused on B2B network services. The deal aimed to combine CenturyLink’s customer base and local access with Level 3’s global fiber network to form a top-tier enterprise connectivity provider. CenturyLink bought Level 3 for $34 billion using a mix of stock and cash, and over $8 billion debt was raised to finance the transaction.

To adapt to the shifting telecom landscape, the company reorganized its portfolio into three categories: ‘Harvest,’ ‘Nurture,’ and ‘Grow.’ The plan was simple in theory: squeeze as much cash as possible from legacy ‘Harvest’ businesses to fund the capital-hungry fiber rollout. The reality, however, was a lot crueler. Legacy copper revenue eroded faster than expected as it collapsed from $5.3 billion in 2018 to just $3.8 billion in 2022. At the same time, investment demands on the growth side ballooned, with capex rising 15% from $3.0 billion in 2018 to $3.7 billion in 2019. Worse yet, the payoff was slow. In 2024, Fiber Broadband revenue increased $99 million YOY, dwarfed by $328 million copper losses in the same consumer segment and another $252 million decline in the “Harvest” business portfolio.

Since 2019, Lumen’s debt and interest expense have surged while revenue has lagged. From 2019 through 2021, operating income fell short of covering interest obligations, and free cash flow turned negative in 2021. By September 2023, the company’s capital structure had become precarious. It faced daunting maturity walls that were difficult to refinance, with $1.3 billion of debt coming due in 2025 and another $7.8 billion maturing in 2027. An out-of-court restructuring seemed to be the best solution.

Since 2019, Lumen’s debt and interest expense have surged while revenue has lagged. From 2019 through 2021, operating income fell short of covering interest obligations, and free cash flow turned negative in 2021. By September 2023, the company’s capital structure had become precarious. It faced daunting maturity walls that were difficult to refinance, with $1.3 billion of debt coming due in 2025 and another $7.8 billion maturing in 2027. An out-of-court restructuring seemed to be the best solution.

Finally, in March 2024, Lumen announced that it had completed a massive liability management exercise tackling $15 billion in debt across 15 tranches. Engineered by Guggenheim, the transaction pushed out the majority of its maturities by five years, with the first of its new notes now due in 2029. In exchange, Lumen agreed to pay an additional $150 million interest to creditors. The transaction was done mostly in the form of debt exchange and extension, with little creditor-on-creditor violence that had become increasingly common, as shown in the cases of Serta, Incora, and many more.

Finally, in March 2024, Lumen announced that it had completed a massive liability management exercise tackling $15 billion in debt across 15 tranches. Engineered by Guggenheim, the transaction pushed out the majority of its maturities by five years, with the first of its new notes now due in 2029. In exchange, Lumen agreed to pay an additional $150 million interest to creditors. The transaction was done mostly in the form of debt exchange and extension, with little creditor-on-creditor violence that had become increasingly common, as shown in the cases of Serta, Incora, and many more.

The liability management exchanges are covered by Pari Passu in detail. Here is a concise summary:

- $1.2 billion new 1L debt secured by Level 3 assets

- $2.4 billion Level 3 Term Loan extended maturity from 2027 to 2029/2030 in exchange for a 0.25% increase in interest rate

- $1.1 billion Level 3 notes exchanged into 10.5% senior secured notes due 2030

- Exchanged $4 B of 2L notes maturing 2027–2029 into new notes of the same maturity with +25 bps coupon, chiefly to loosen covenants for future asset sales and exchanges.

- Introduced a new super-priority revolver, while transferring 49% of Qwest assets out, raising Qwest leverage and default risk.

- $5 billion term loans maturing 2025/27 exchanged into a super-priority term loan maturing 2029/30.

- Refinanced $1.75 B of 5.125% 2026 and 4% 2027 notes into $1 B of 4.25% super-priority notes due 2029/30.

Takeaways

The restructuring of CommScope and Lumen illustrates what it means to have a thin margin of error when operating in a capital-intensive industry in decline: CommScope and Lumen, even when they were in distress, were not “bad businesses” at all. Rather, they consistently generated over $5 billion in sales, provided mission-critical products, and were considered to be leading players in their verticals. Yet, their cash-flow-generating capacity no longer supported the debt they had taken on in better times. That imbalance proved decisive.

One thing that stood out to me is that, once a company assumes significant leverage, the obligation to service and refinance that debt persists for years. Hence, while Debt may look attractive especially for telecom companies that need large amounts of upfront capital, it’s more than a cheap source of funds. It’s a long-term choice that has to survive changes in technology, competition, and regulation.

I also came away thinking about the risk of buying your way into a new market. Facing the paradigm shift in the telecommunications industry, both companies decided to make a major acquisition to diversify and stay relevant. Compared with developing new technology in-house, acquisitions can seem more efficient and avoid the uncertainty of home-grown R&D, but the strategy carries its own dangers.

The acquisition could be directionally wrong. CommScope illustrates this perfectly. It paid a significant premium to enter the network equipment market, whose promised growth never materialized. Instead, the deal compressed margins and saddled the balance sheet with debt, ultimately forcing CommScope to sell its once-core infrastructure division just as demand for data-center fiber surged. Even a directionally correct acquisition can threaten survival. Lumen’s purchase of Level 3 was strategically sound, but the heavy leverage left little room for error. When legacy copper revenues fell faster than expected and growth segments scaled more slowly, the debt burden became unsustainable.

Overall, these cases suggest that in industries undergoing seismic change, a company’s capital structure can be just as important as its growth plans. Ambitious deals only work if the balance sheet can handle unexpected setbacks, and that’s a lesson I’ll keep in mind as I continue learning about restructuring and how companies navigate different market cycles.